All Categories

Featured

Table of Contents

The technique has its own advantages, however it additionally has problems with high charges, intricacy, and much more, resulting in it being concerned as a scam by some. Limitless banking is not the most effective plan if you require only the investment part. The unlimited financial idea revolves around making use of entire life insurance policy plans as a financial tool.

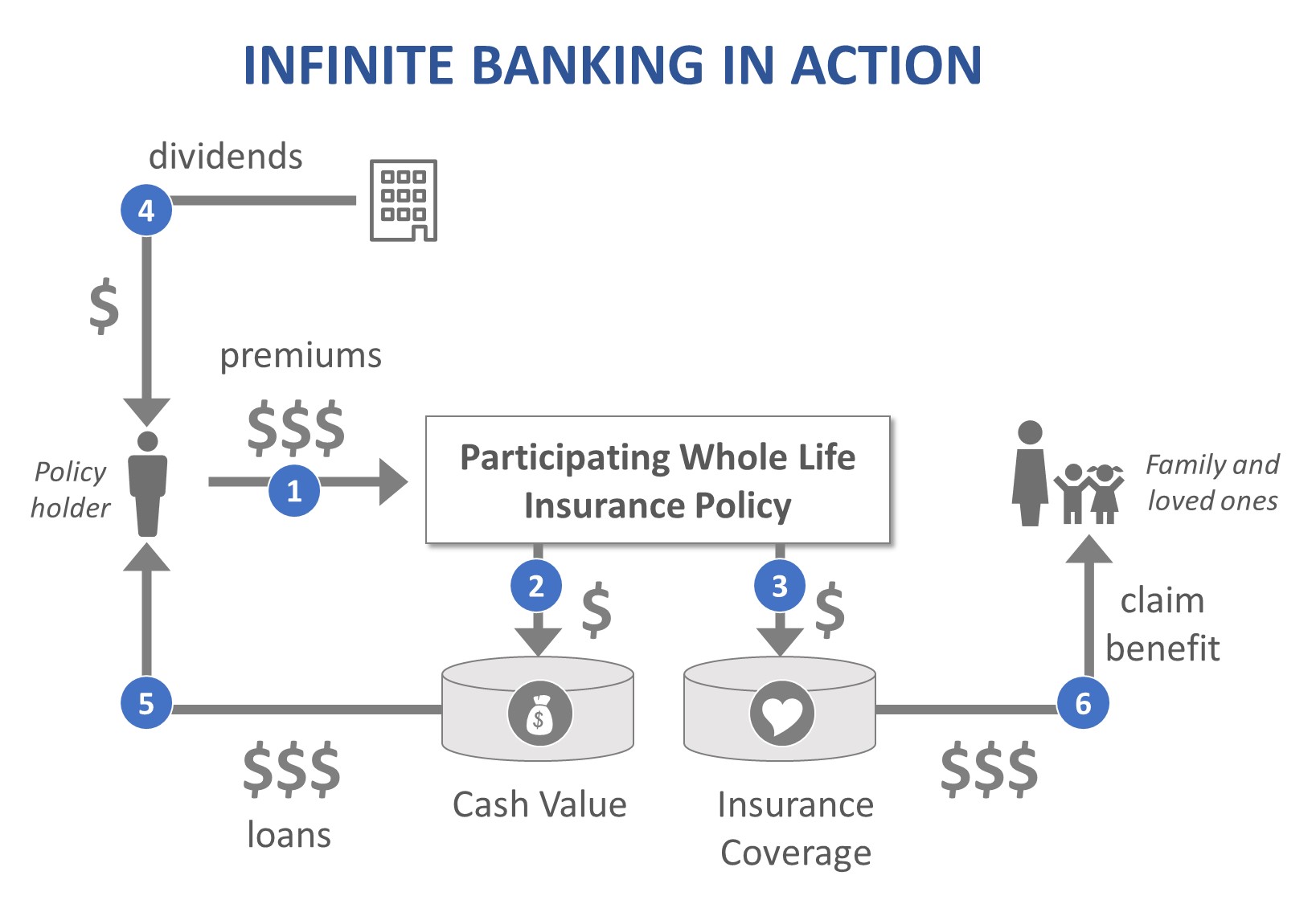

A PUAR allows you to "overfund" your insurance plan right up to line of it ending up being a Changed Endowment Contract (MEC). When you make use of a PUAR, you swiftly raise your money value (and your death benefit), consequently enhancing the power of your "bank". Even more, the even more cash money value you have, the better your passion and returns settlements from your insurance coverage business will be.

With the increase of TikTok as an information-sharing system, monetary advice and approaches have located a novel way of dispersing. One such method that has been making the rounds is the infinite banking idea, or IBC for brief, gathering endorsements from stars like rap artist Waka Flocka Flame - Cash value leveraging. Nonetheless, while the approach is presently prominent, its origins trace back to the 1980s when financial expert Nelson Nash introduced it to the world.

How does Whole Life For Infinite Banking compare to traditional investment strategies?

Within these plans, the money value expands based upon a rate established by the insurer. As soon as a considerable money value gathers, insurance policy holders can obtain a money value finance. These financings differ from traditional ones, with life insurance policy serving as collateral, indicating one might lose their insurance coverage if borrowing excessively without sufficient cash money worth to support the insurance coverage expenses.

And while the attraction of these policies appears, there are innate limitations and dangers, demanding attentive cash money value surveillance. The method's legitimacy isn't black and white. For high-net-worth individuals or entrepreneur, especially those utilizing methods like company-owned life insurance coverage (COLI), the advantages of tax breaks and substance growth might be appealing.

The allure of limitless financial does not negate its challenges: Expense: The foundational requirement, a permanent life insurance plan, is more expensive than its term counterparts. Qualification: Not everybody receives entire life insurance policy as a result of extensive underwriting processes that can exclude those with certain health or way of life conditions. Complexity and risk: The complex nature of IBC, combined with its dangers, might discourage lots of, especially when easier and less risky options are available.

How secure is my money with Policy Loan Strategy?

Designating around 10% of your monthly earnings to the plan is simply not possible for many people. Using life insurance policy as a financial investment and liquidity resource needs self-control and tracking of plan cash value. Seek advice from an economic consultant to determine if limitless banking straightens with your concerns. Component of what you read below is just a reiteration of what has currently been stated over.

So prior to you obtain right into a circumstance you're not prepared for, know the following initially: Although the principle is commonly sold thus, you're not in fact taking a financing from on your own. If that were the instance, you wouldn't need to settle it. Instead, you're borrowing from the insurance provider and need to settle it with passion.

Some social networks posts recommend utilizing money worth from entire life insurance policy to pay down credit card financial debt. The idea is that when you pay back the finance with rate of interest, the quantity will be sent out back to your investments. Sadly, that's not how it functions. When you pay back the car loan, a portion of that passion mosts likely to the insurance provider.

What are the common mistakes people make with Infinite Banking?

For the initial a number of years, you'll be settling the compensation. This makes it extremely hard for your plan to accumulate worth throughout this time. Whole life insurance policy costs 5 to 15 times more than term insurance policy. Lots of people merely can't manage it. So, unless you can pay for to pay a few to a number of hundred dollars for the next decade or even more, IBC will not help you.

Not everybody should rely exclusively on themselves for economic security. Infinite Banking vs traditional banking. If you call for life insurance policy, here are some beneficial pointers to take into consideration: Consider term life insurance. These plans supply insurance coverage during years with considerable economic commitments, like mortgages, trainee lendings, or when caring for children. Make sure to search for the finest price.

How do I leverage Financial Leverage With Infinite Banking to grow my wealth?

Imagine never ever having to worry concerning bank car loans or high interest rates again. That's the power of infinite banking life insurance.

There's no collection lending term, and you have the flexibility to select the payment schedule, which can be as leisurely as paying back the lending at the time of death. This adaptability encompasses the servicing of the car loans, where you can go with interest-only payments, maintaining the funding equilibrium level and manageable.

Financial Leverage With Infinite Banking

Holding cash in an IUL dealt with account being credited passion can commonly be much better than holding the cash on deposit at a bank.: You have actually always imagined opening your own bakery. You can borrow from your IUL plan to cover the preliminary expenses of leasing an area, buying equipment, and employing personnel.

Personal loans can be gotten from traditional banks and credit rating unions. Borrowing money on a debt card is usually extremely pricey with annual percent prices of rate of interest (APR) frequently reaching 20% to 30% or more a year.

{kind=link}

Latest Posts

Be Your Own Bank: 3 Secrets Every Saver Needs

Infinite Banking Review

Infinite Banking Concept Life Insurance